GROUP_MOVING_AVERAGE

Syntax

GROUP_MOVING_AVERAGE(<number>;[<number>])

Values: time series values

K: number of past values to compute the moving average from

Description

This function smooths a time series by applying a simple moving average of the past k values. Smoothing a time series helps remove random noise and leave the user with a general trend. You might use GROUP_HOLT_WINTERS for exponential smoothing.

This is an aggregate function.

Example

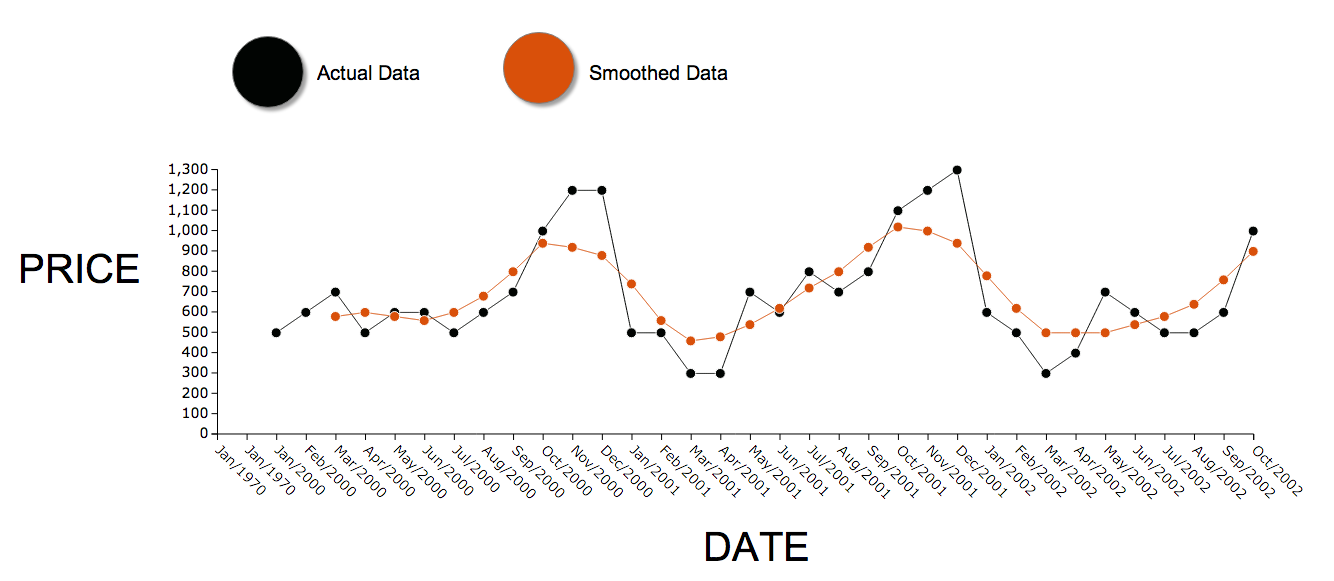

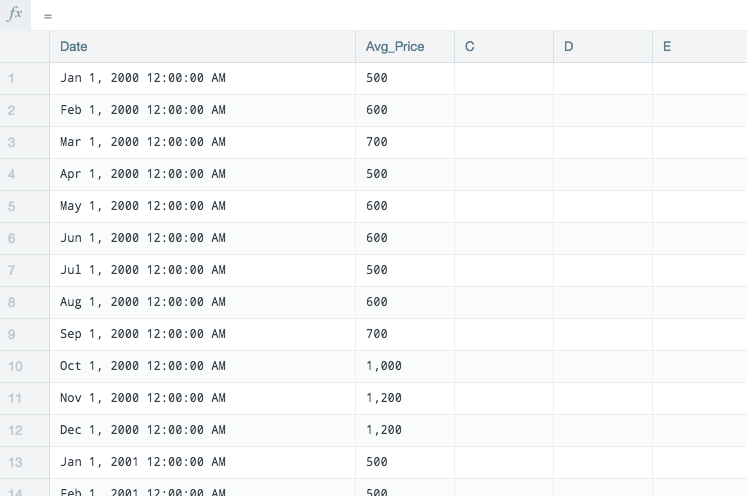

In the following example you have average stock price values per month over a three year period. Try to smooth the data to find the general trend.

Next, duplicate this source into a calculation sheet in order to work on it.

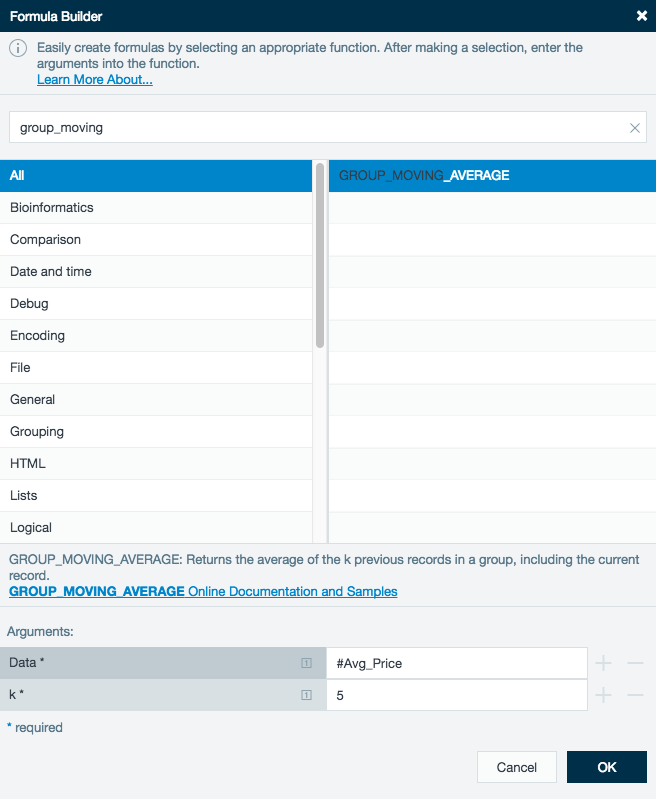

Click an empty column to bring up the Formula Builder (As of Datameer v6.4, click the Fx button on the formula line to display the formula builder) and select GROUP_MOVING_AVERAGE

Use the Avg_Price as the Data and set the k at 5. This uses each previous 5 months to create a smoothed average for each data record.

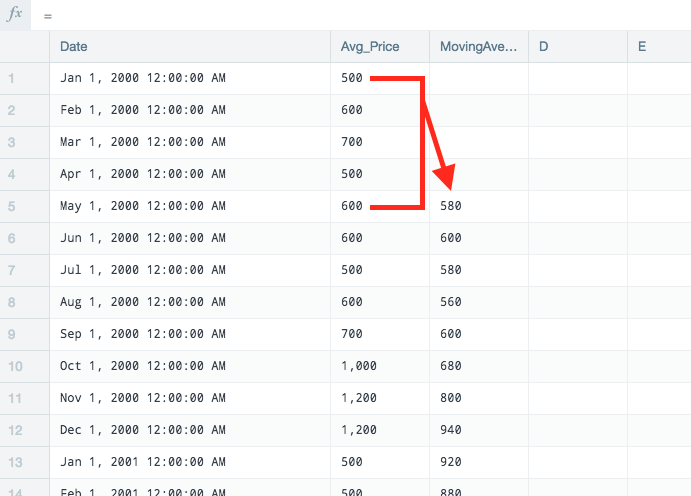

The first record in the column MovingAverage_Price_5 is an average of the first 5 records of Avg_Price.

As the Moving_Average_Price_5 records are the average of the previous 5 Avg_Price records, the Moving_Average needs to match to the median of the Date and Ave_Price.

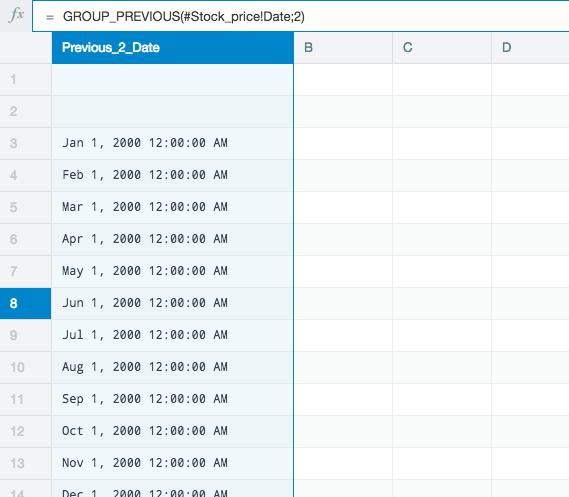

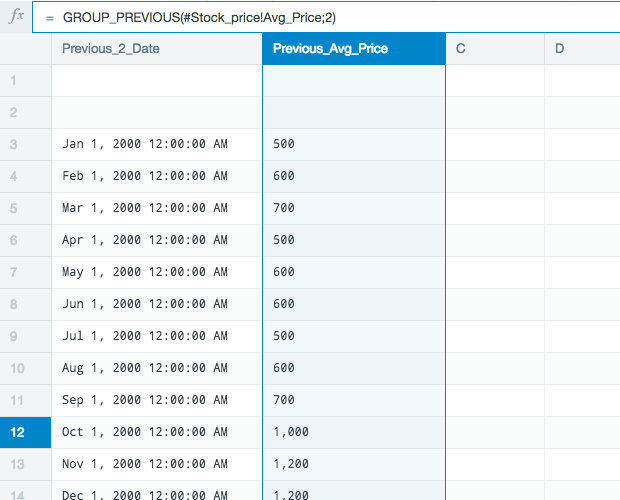

Create a new sheet and click the first open column to bring up the Formula Builder. Select GROUP_PREVIOUS to shift the Date column down two rows.

Use the same GROUP_PREVIOUS function to shift the Avg_Price down by two rows.

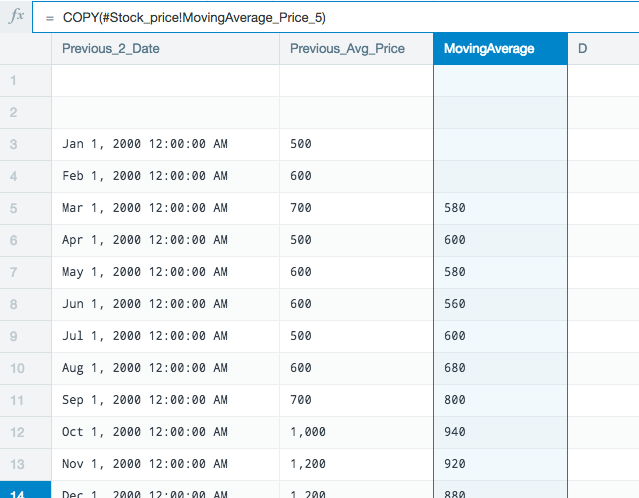

Finally, COPY the MovingAverage_Price_5 into the sheet.

The moving average values are now properly aligned with the median date and price the moving average is based on.

After having completed the workbook, a line chart would be a good tool to visualize your new smoothed data compared to your actual data.